Over the last year, we've spent time trying to understand the biggest bottlenecks in emerging market lending. A large part of the conversation in fintech has rightly focused on foundational infrastructure, as we do so in our recently published report on The Philippine Fintech Stack. But the more time we spent with lenders across the region, the clearer it became that even when data exists, lending decisions are still constrained at the operational layer: the documents, workflows, and manual review processes sitting between raw information and actual credit deployment.

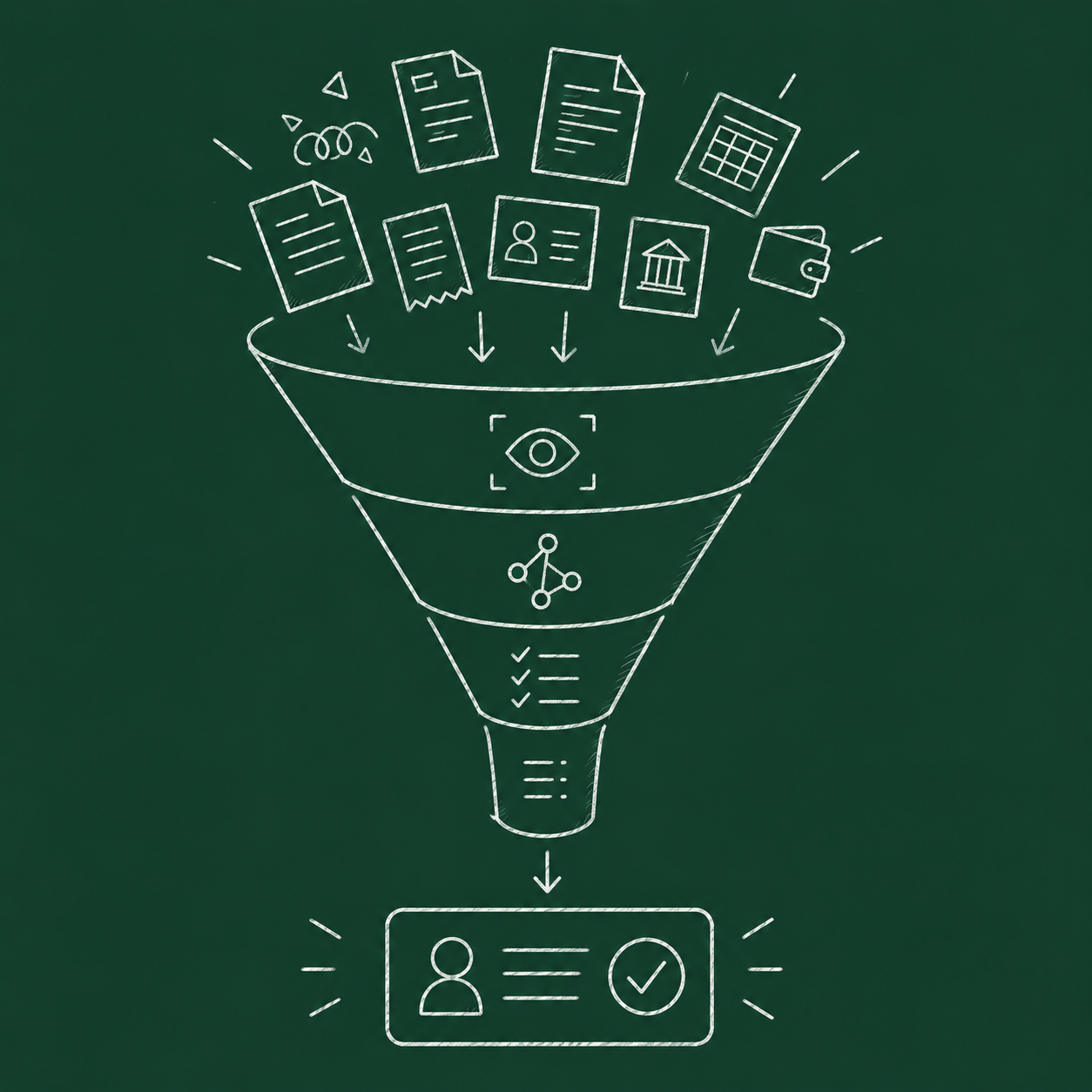

Indeed, lending in emerging markets still runs on documents. Every loan decision—be it a $200 microloan to a consumer or a $50,000 SME line—routes through a credit officer manually reviewing a stack of files. Bank statements scanned unclearly. Payslips photographed in low light. Handwritten ledgers and screenshots of e-wallet histories, all in inconsistent formats.

The average review takes around four hours per file and a full credit committee turnaround can stretch from weeks to months. OCR tools built for standardized U.S. documents fall apart on real-world emerging market inputs. Fraud quietly slips through. Underwriting decisions vary across reviewers. To manage the load, lenders cap their loan volumes which often leaves qualified borrowers underserved or pushed toward predatory alternatives.

In 2025, $13.3T was lent globally, with roughly 90% of those transactions involving some form of document review. The fastest growing lending markets in the world are exactly the ones with the weakest credit infrastructure: South America (12.3% CAGR), Africa (10.3%), and Asia-Pacific (13.2%) all outpacing the global average.

Kita is building the document intelligence layer for emerging market lending. Using vision-language model (VLM) agents, they automate everything a credit officer does today: parsing dozens of document types, detecting fraud, cross-checking data, and extracting structured financial signals ready for underwriting. What does this mean in practice? Review time drops from four hours to minutes, loan turnaround moves from months to same-day, and the same credit team can underwrite five times more loans without scaling headcount.

The product is delivered two ways: as an API embedded directly into a lender's loan origination system and as a web portal for credit officers without engineering bandwidth.

Developments over the last two years make today the right time for a solution like Kita:

We get excited about founders who are building for emerging markets and who also have the technical depth to execute properly. Carmel Limcaoco and Rhea Malhotra are exactly the kind of pairing we look for.

Carmel, born and raised in Manila, worked at Apple under the Product Management team for three summers and was a UN Awardee by the age of 16. She finished her undergraduate studies at Stanford, and while there, helped launch and organize the Kaya Founders Product Design Fellowship. Her network across the fintech ecosystem has been a meaningful part of why Kita has been able to move quickly into the right customer conversations.

Rhea is one of the most technically credentialed founders we've come across. She received the Firestone Medal, the single highest honor in Stanford's Computer Science department in 2025, and is a seven-time published AI researcher in computer vision.

What gives Kita long-term defensibility is the data flywheel. Every customer relationship deepens a proprietary dataset of documents linked to actual repayment outcomes — a dataset frontier model providers don't see and that API-first competitors won't build. Over time, that data becomes the foundation for something much larger than document parsing: a real understanding of what actually predicts repayment in emerging markets.

This investment fits squarely within our Embedded Credit thesis. We've been consistent in our view that the next wave of category leaders in Southeast Asian fintech will be the ones building foundational infrastructure. Kita is exactly that: the data layer underneath everything else, with a roadmap that extends naturally into origination, underwriting, and decisioning over time.

We're proud to be the only Philippine-based venture capital investor on Kita's cap table, alongside a group of Silicon Valley-based VCs. We're betting that Kita becomes the credit infrastructure layer that emerging market lending is built on and we're excited to partner with Carmel and Rhea for the ride.